A customer is at your checkout, whether physical or virtual. They are ready to pay. The ease, speed, and familiarity of that final step will be their lasting impression of your brand.

For Singaporean businesses, this presents a unique puzzle. The payment landscape is a blend of deeply ingrained habits and cutting-edge technology: traditional credit card usage remains strong, a national real-time payment network (PayNow) has achieved near-universal adoption, and a dominant super-app wallet (GrabPay) commands immense loyalty.

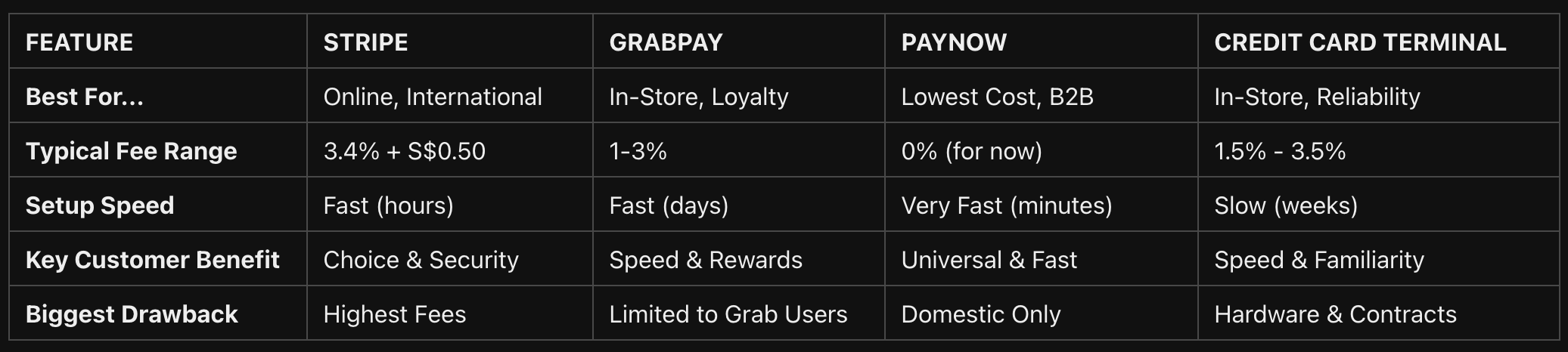

Navigating these choices can be overwhelming. To help you make a clear decision, we’re putting the four main contenders head-to-head. We'll dissect Stripe, the global engine for online commerce; GrabPay, the everyday e-wallet; PayNow, the ubiquitous national standard; and the reliable Credit Card Terminal. This guide will break down each option by the three factors that matter most to an SME: Transaction Fees, Integration Ease, and Customer Experience.

Who It's Best For

E-commerce stores, SaaS businesses, platforms, and any business that needs a powerful, flexible online payment processing system, especially those serving an international audience.

Transaction Fees

Stripe’s pricing is transparent and comprehensive. The standard rate for most local card transactions is 3.4% + S$0.50. This fee might seem higher than other options, but it bundles the payment gateway, processing, and a suite of powerful developer tools. Accepting other wallets through Stripe has its own rates, such as 3.3% for GrabPay. Be mindful of extra costs for international cards (+0.5%) and currency conversion (+2%), which are critical considerations for businesses selling globally.

Ease of Integration

Stripe’s flexibility is its greatest strength. For those without technical skills, Stripe Payment Links and Checkout allow you to create instant payment pages with just a few clicks. For businesses built on major platforms like Shopify or WooCommerce, Stripe offers seamless, low-code integrations. Their robust APIs and world-class documentation make it a favourite among developers for building custom solutions.

Customer Experience

For customers, Stripe offers a professional and secure checkout experience. Its ability to accept a wide variety of payment methods from around the world makes it a reliable choice for international shoppers. The main drawback is that it can involve more steps (like manually entering card details) compared to a simple QR code scan, which might feel slightly slower for local, mobile-first users.

Who It's Best For

F&B outlets, retail stores, and businesses targeting a mobile-first, younger demographic that is heavily invested in the Grab ecosystem.

Transaction Fees

GrabPay’s merchant fees are typically negotiated directly with the business but generally fall within the 1-3% range. The key here is to look beyond the percentage. The fee is your ticket to accessing millions of active Grab users and Grab's loyalty program, GrabRewards. Customers are often incentivised to use GrabPay to earn points, which can drive traffic to your business.

Ease of Integration

For in-store businesses, integration is incredibly simple. It often involves just displaying a GrabPay QR code, which is usually part of the unified SGQR code, allowing for a clean and uncluttered countertop. For online stores, integration is possible through various payment aggregators or on supported e-commerce platforms.

Customer Experience

For a Grab user, paying with GrabPay is extremely fast and convenient. The ability to earn and spend GrabRewards points is a major driver of adoption and can be a significant competitive advantage. However, its strength is also its weakness: for customers who are not part of the Grab ecosystem, this payment option is entirely irrelevant.

Who It's Best For

Every single business in Singapore. From hawker stalls and B2C service providers to B2B companies sending invoices, PayNow is the universal baseline for collecting payments locally.

Transaction Fees

This is PayNow’s superpower. For businesses, receiving payments via PayNow comes with extremely low to zero fees. Many major banks in Singapore are offering free inward PayNow transactions for businesses until the end of 2025, making it by far the most cost-effective way to collect payment in Singapore dollars.

Ease of Integration

The setup process is remarkably straightforward. A business simply needs to link its corporate bank account to its Unique Entity Number (UEN). From there, you can generate a static PayNow QR code to display in-store or on your website, or a dynamic one for individual invoices.

Customer Experience

PayNow boasts massive adoption. Almost every Singaporean with a banking app can use it instantly, with no new app downloads required. It’s seen as secure, direct, and incredibly fast. The only real limitation is that it’s primarily a domestic solution and lacks the rich data and analytics features that come with a dedicated payment platform like Stripe.

Who It's Best For

Established brick-and-mortar retailers, high-volume F&B establishments, and any business where customers, including tourists, have a strong expectation to tap-and-go with their physical cards.

Transaction Fees

Fees for card terminals are the most complex, typically ranging from 1.5% to 3.5%. The exact rate depends heavily on your provider, your monthly transaction volume, and the types of cards your customers use. Always be sure to ask about associated costs like monthly terminal rental fees or one-time setup charges.

Ease of Integration

Setting up requires physical hardware and usually involves signing a contract with a bank or a merchant acquirer. The process is generally more formal and can be slower than setting up digital-first options.

Customer Experience

The tap-to-pay experience is universally understood, trusted, and incredibly fast for in-person transactions. It’s the most straightforward way to accept payments from tourists and customers who may not use local payment apps. The main drawback is its lack of flexibility for online businesses and the need to manage physical hardware.

If you're an online e-commerce store...

Use Stripe as the primary engine for its robust features and global reach. Add PayNow as a manual payment option at checkout to provide a low-cost alternative for local buyers.

If you're a busy CBD cafe...

A modern Credit Card Terminal is essential for speed at the counter. Combine it with a single SGQR code that accepts both PayNow and GrabPay to cater to every type of office worker.

If you're a B2B consulting firm...

PayNow is king for local invoicing due to its zero/low fees. Use Stripe Payment Links for international clients who prefer to pay by card.

If you're a neighbourhood retail shop...

Use a Credit Card Terminal for card-present customers, especially tourists. A prominent PayNow QR code at the counter for cost-conscious, local transactions.

The winning payment strategy in 2025 is rarely about choosing a single provider. You'll have to create hybrid approach that offers flexibility for your customers and makes financial sense for your business. Don't force your customers into one box when you can easily cater to their preferences.

To guide your decision, remember the core strengths:

Take a look at your current payment options. Is there a gap? Is there a way to make it easier for your customers and more cost-effective for you? The right answer could be your next competitive advantage.